SP500 Robert Shiller's data set for U.S. Stock Markets 1871–2021 and CAPE Ratio.

data(SP500)Format

An xts object containing observations of U.S. Stock Markets

1871–Present and CAPE Ratio.

- **Frequency:**

Monthly

- **Date Range:**

1871-01 to 2023-09

- **SP500:**

Nominal prices of the S&P composite index, April 2021 observation is 04/05 close

- **Dividends:**

Nominal dividends

- **Earnings:**

Nominal earnings, S&P 500 estimated

- **CPI:**

Shiller's Consumer Price Index data used for transformation to real prices

- **GS10:**

Shiller's Long-term interest rate, 10-Year Treasury Constant Maturity Rate, April 2021 observation is 04/05 close

- **Real_SP500:**

Real prices of the S&P 500 composite index

- **Real_Dividends:**

Real dividends

- **Real_SP500_TR:**

Real total return price of the S&P 500 composite index

- **Real_Earnings:**

Real earnings

- **Real_Earnings_TR:**

Real total return scaled earnings

- **CAPE:**

Cyclically Adjusted Price Earnings Ratio (P/E10 or CAPE)

- **CAPE_TR:**

Cyclically Adjusted Total Return Price Earnings Ratio (P/E10_TR or CAPE_TR)

- **CAPE_Yield:**

Excess CAPE Yield

- **Bond_TR:**

Total bond returns

- **Real_Bond_TR:**

Real total bond returns

Source

Shiller, Robert J. *Irrational Exuberance*, Princeton University Press 2000, Broadway Books 2001, 2nd ed. 2005, 3rd ed. 2015. http://www.econ.yale.edu/~shiller/data.htm

Download .xls file directly from here: http://www.econ.yale.edu/~shiller/data/ie_data.xls

Notes from Shiller

This data set consists of monthly stock price, dividends, and earnings data and the consumer price index (to allow conversion to real values), all starting January 1871. The price, dividend, and earnings series are from the same sources as described in Chapter 26 of my earlier book (Market Volatility, Cambridge, MA: MIT Press, 1989), although now I use monthly data, rather than annual data.

Monthly dividend and earnings data are computed from the S&P four-quarter totals for the quarter since 1926, with linear interpolation to monthly figures. Dividend and earnings data before 1926 are from Cowles and associates (Common Stock Indexes, 2nd ed., Bloomington, Ind.: Principia Press, 1939), interpolated from annual data. Stock price data are monthly averages of daily closing prices.

The CPI-U (Consumer Price Index–All Urban Consumers) published by the U.S. Bureau of Labor Statistics begins in 1913; for years before 1913, Shiller spliced Warren and Pearson's price index by multiplying it by the ratio of the indexes in January 1913. December 1999 and January 2000 values for the CPI-U are extrapolated. See George F. Warren and Frank A. Pearson, *Gold and Prices* (New York: John Wiley and Sons, 1935). Data are from their Table 1, pp. 11–14.

Examples

data(SP500)

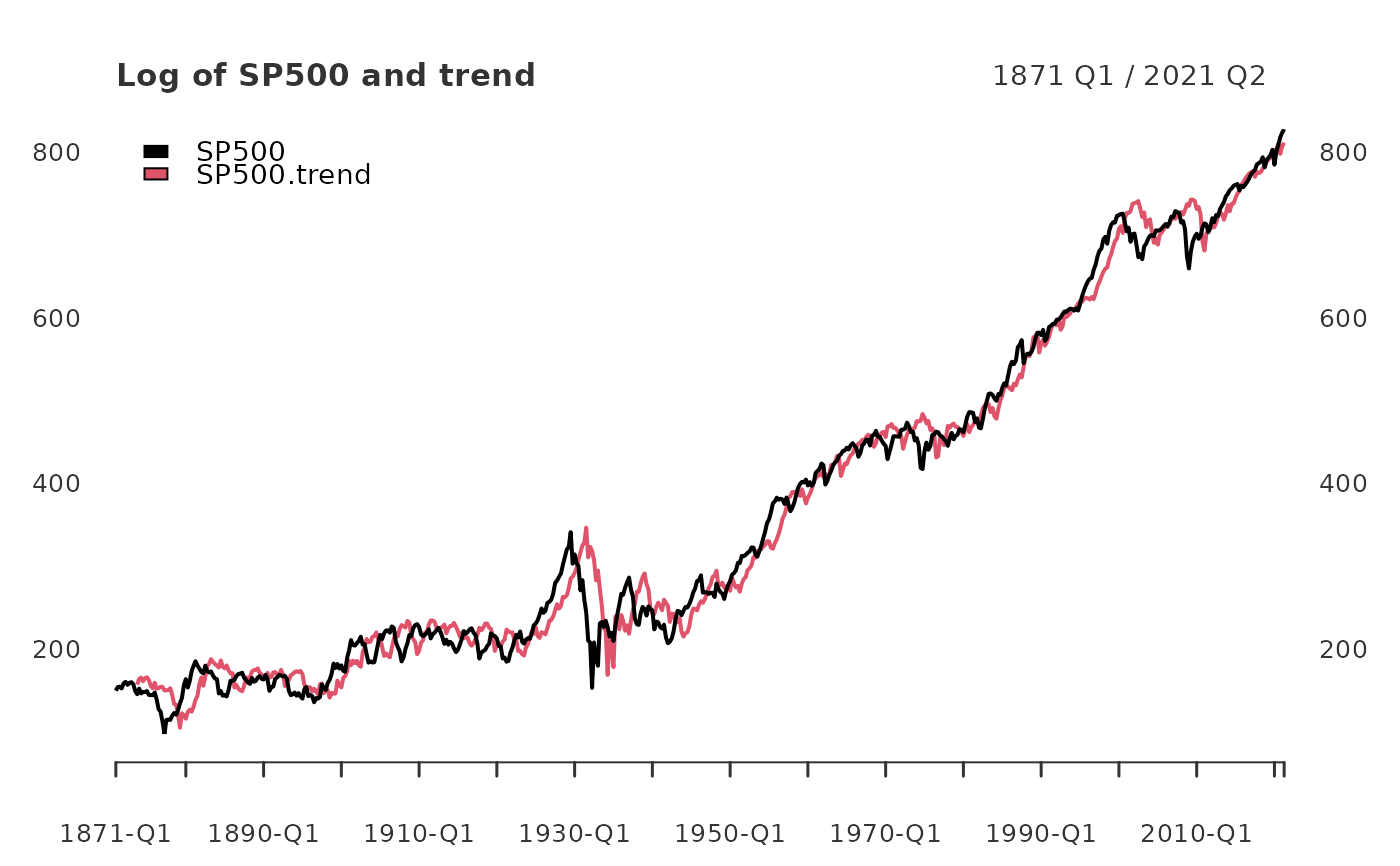

SP500_qtr <- xts::to.quarterly(SP500$SP500, OHLC = FALSE)

log_SP500 <- 100*log(SP500_qtr)

SP500_trend <- yth_filter(log_SP500, h = 8, p = 4,

output = c("x", "trend"), family = gaussian)

main <- "Log of SP500 and trend"

plot(SP500_trend, grid.col = "white", legend.loc = "topleft", main = main)

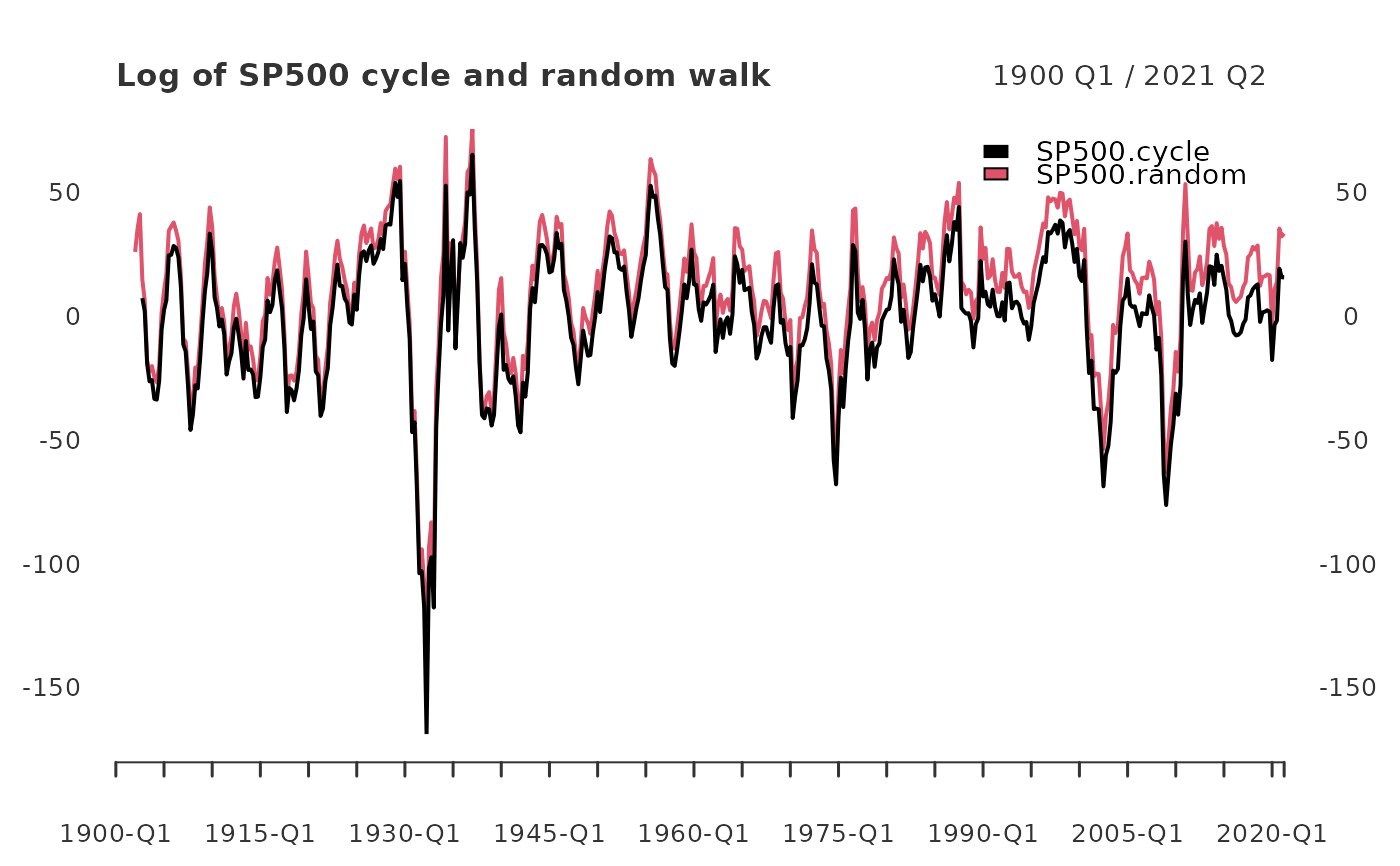

SP500_cycle <- yth_filter(log_SP500["1900/"], h = 8, p = 4,

output = c("cycle", "random"), family = gaussian)

main <- "Log of SP500 cycle and random walk"

plot(SP500_cycle, grid.col = "white", legend.loc = "topright", main = main)

SP500_cycle <- yth_filter(log_SP500["1900/"], h = 8, p = 4,

output = c("cycle", "random"), family = gaussian)

main <- "Log of SP500 cycle and random walk"

plot(SP500_cycle, grid.col = "white", legend.loc = "topright", main = main)