yth_glm fits a generalized linear model suggested by James D. Hamilton

as a better alternative to the Hodrick-Prescott Filter.

yth_glm(x, h = 8, p = 4, ...)Arguments

- x

A univariate

xtsobject of anyzooindex class, such asDate,yearmon, oryearqtr. For converting objects of typetimeSeries,ts,irts,fts,matrix,data.frame, orzootoxts, please seeas.xts.- h

An

integer, defining the lookahead period. Defaults toh = 8, suggested by Hamilton. The default assumes economic data of quarterly periodicity with a lookahead period of 2 years. This function is not limited by the default parameter, and econometricians may change it as required.- p

An

integer, indicating the number of lags. A default ofp = 4, suggested by Hamilton, assumes data is of quarterly periodicity. If data is monthly, one may choosep = 12or aggregate the series to quarterly and maintain the default. Econometricians should use this parameter to accommodate the seasonality of their data.- ...

Additional arguments passed to

glm.

Details

For time series of quarterly periodicity, Hamilton suggests parameters of h = 8 and p = 4, or an \(AR(4)\) process, additionally lagged by \(8\) lookahead periods. Econometricians may explore variations of h. However, p is designed to correspond with the seasonality of a given periodicity and should be matched accordingly.

References

James D. Hamilton. Why You Should Never Use the Hodrick-Prescott Filter. NBER Working Paper No. 23429, Issued in May 2017.

Examples

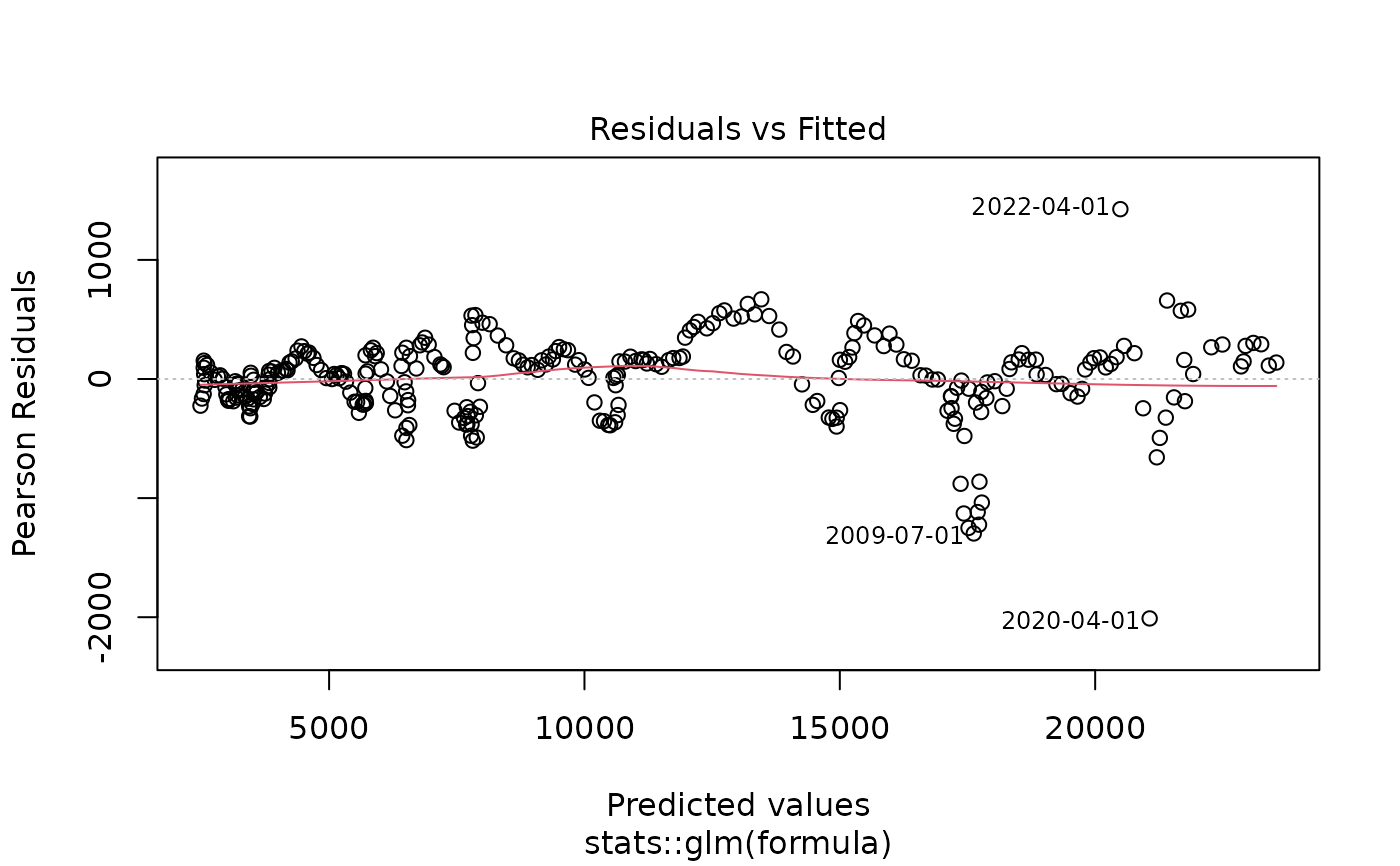

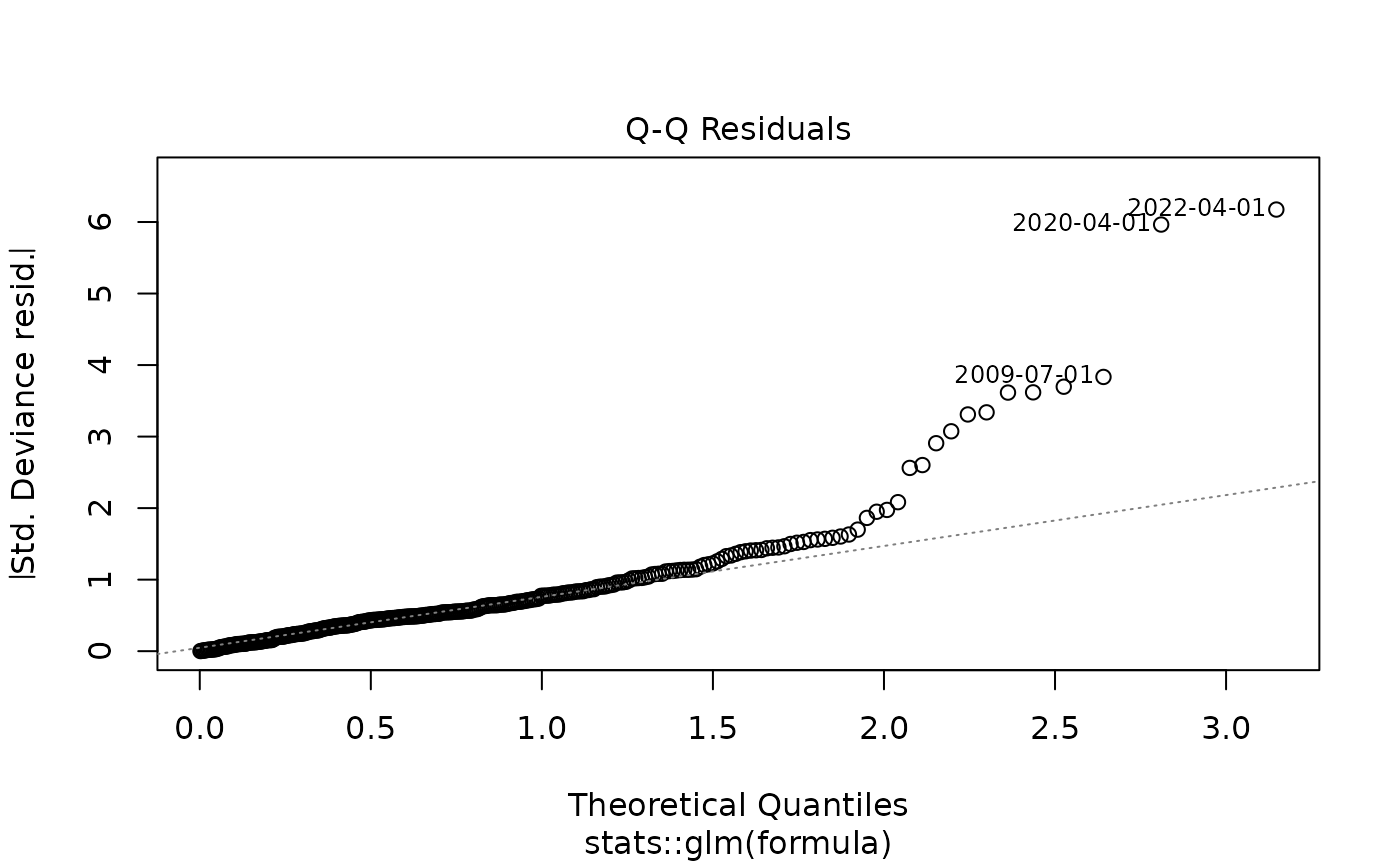

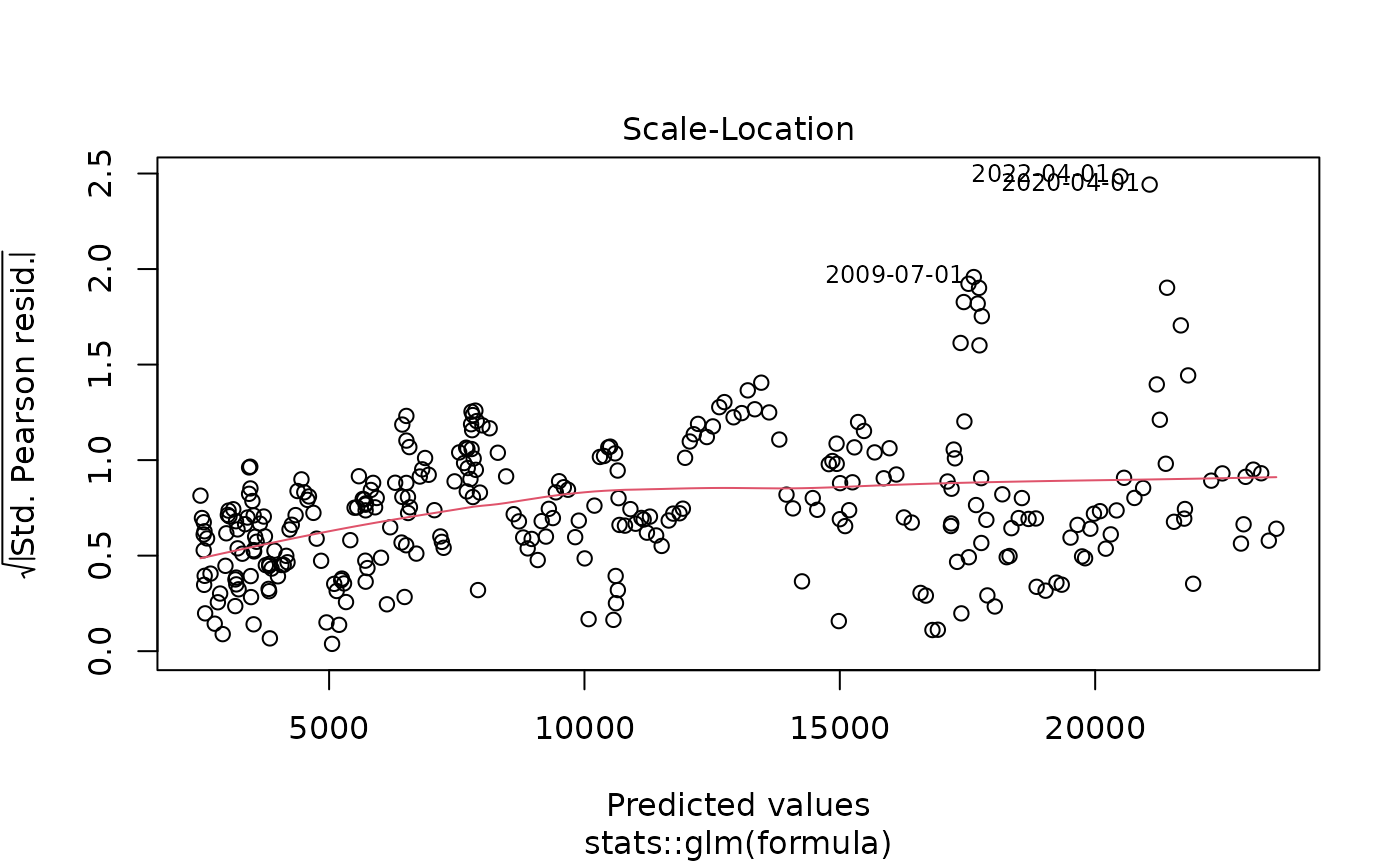

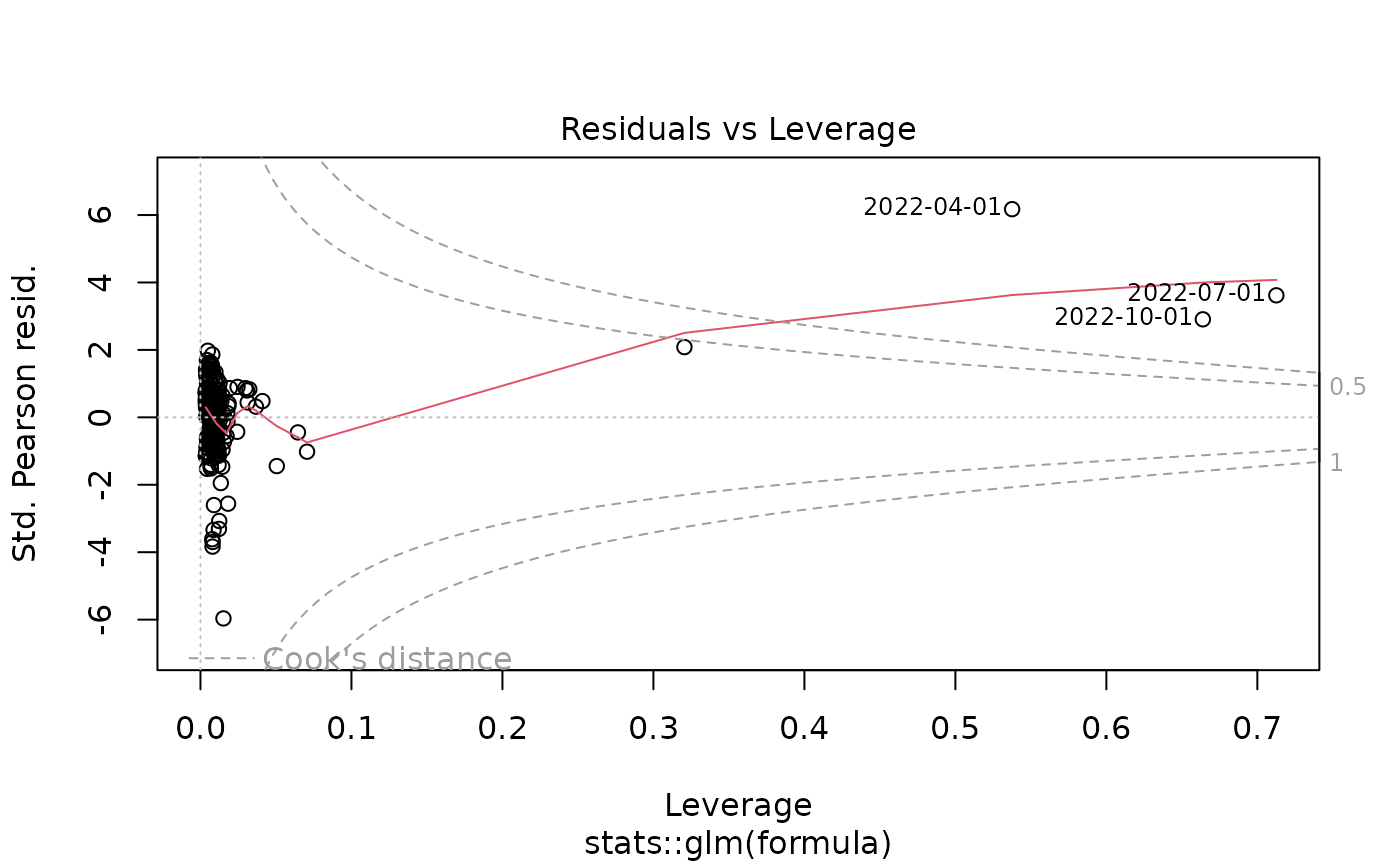

data(GDPC1)

gdp_model <- yth_glm(GDPC1, h = 8, p = 4, family = gaussian)

summary(gdp_model)

#>

#> Call:

#> stats::glm(formula = formula, family = ..1, data = data)

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 195.9049 38.3005 5.115 5.63e-07 ***

#> xt_0 0.7590 0.1321 5.746 2.26e-08 ***

#> xt_1 0.1344 0.1729 0.778 0.437

#> xt_2 0.0431 0.1729 0.249 0.803

#> xt_3 0.1030 0.1327 0.777 0.438

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> (Dispersion parameter for gaussian family taken to be 115351.3)

#>

#> Null deviance: 1.1636e+10 on 302 degrees of freedom

#> Residual deviance: 3.4375e+07 on 298 degrees of freedom

#> (11 observations deleted due to missingness)

#> AIC: 4398.5

#>

#> Number of Fisher Scoring iterations: 2

#>

plot(gdp_model)