Introductory Econometrics Examples

Justin M Shea

Source:vignettes/Introductory-Econometrics-Examples.Rmd

Introductory-Econometrics-Examples.RmdIntroduction

This vignette reproduces examples from various chapters of Introductory Econometrics: A Modern Approach, 7e by Jeffrey M. Wooldridge. Each example illustrates how to load data, build econometric models, and compute estimates with R.

In addition, the Appendix cites a few sources using

R for econometrics. Of note, in 2020 Florian Heiss

published a 2nd edition of Using R

for Introductory Econometrics; it is excellent. The Heiss text

is a companion to wooldridge for R users, and offers an in

depth treatment with several worked examples from each chapter. Indeed,

his example use this wooldridge package as well.

Now, install and load the wooldridge package and lets

get started!

install.packages("wooldridge")Chapter 2: The Simple Regression Model

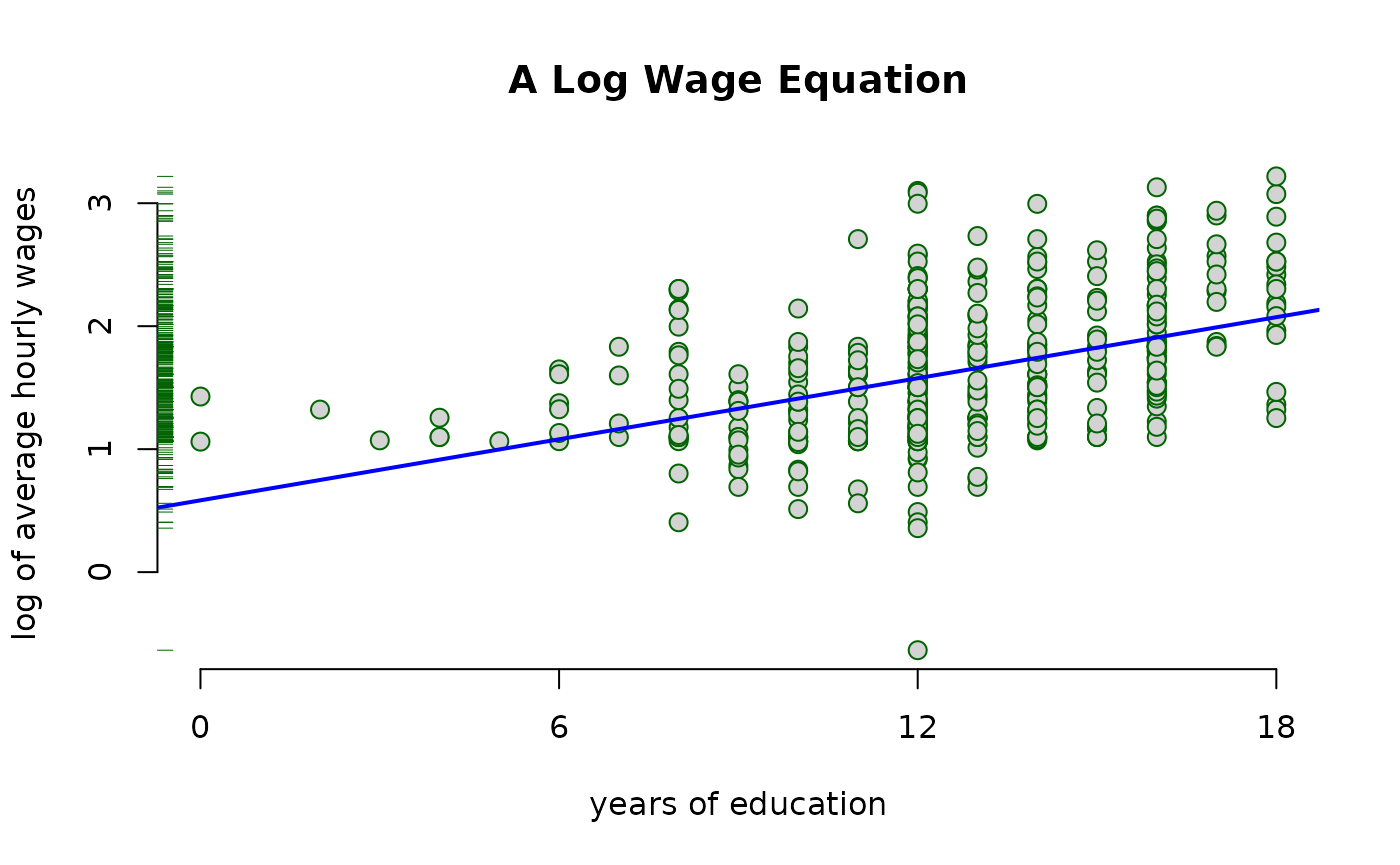

Example 2.10: A Log Wage Equation

Load the wage1 data and check out the documentation.

data("wage1")

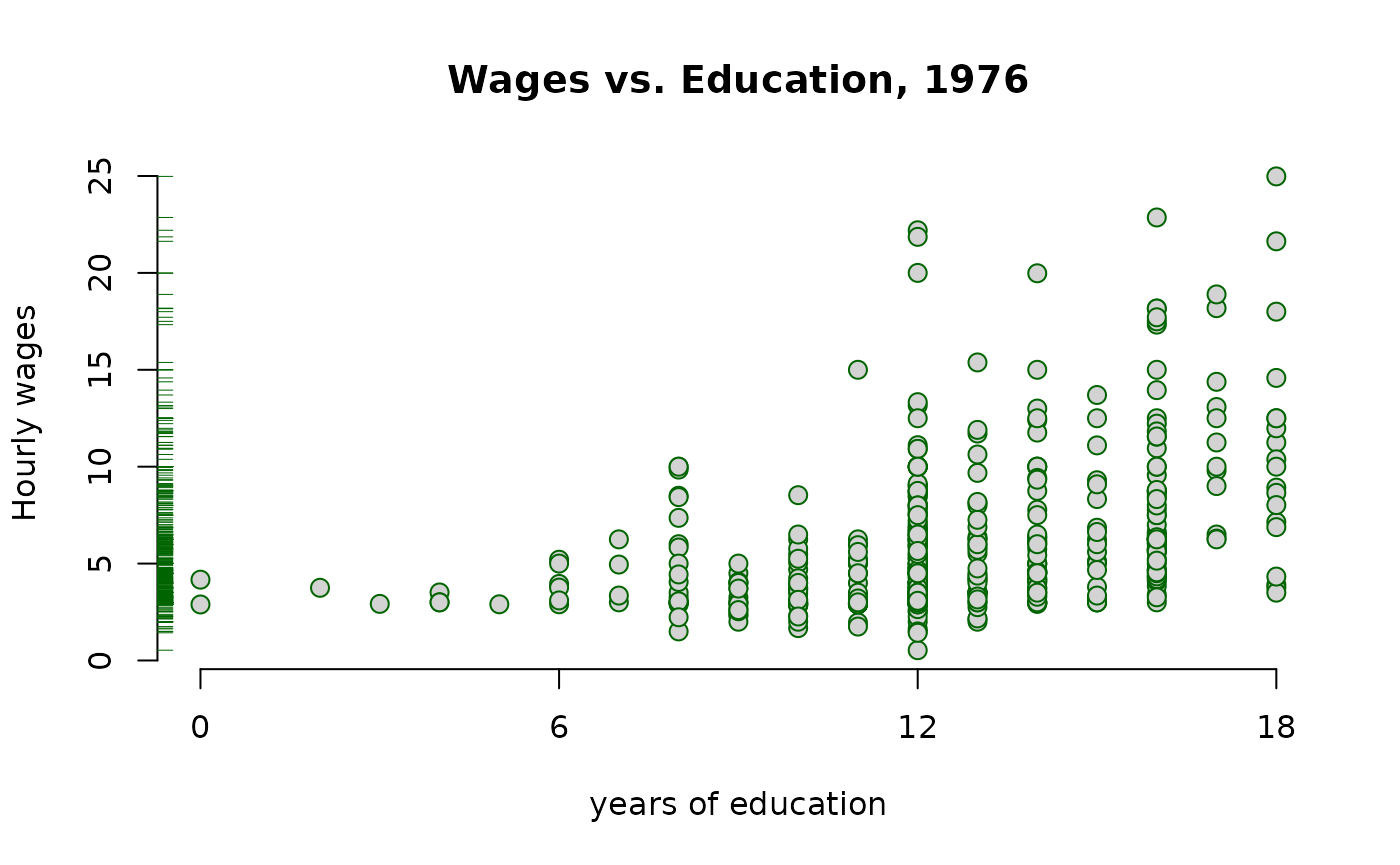

?wage1The documentation indicates these are data from the 1976 Current Population Survey, collected by Henry Farber when he and Wooldridge were colleagues at MIT in 1988.

: years of education

: average hourly earnings

: log of the average hourly earnings

First, make a scatter-plot of the two variables and look for possible patterns in the relationship between them.

It appears that on average, more years of education, leads to higher wages.

The example in the text is interested in the return to another

year of education, or what the percentage

change in wages one might expect for each additional year of education.

To do so, one must use the

wage.

This has already been computed in the data set and is defined as

lwage.

The textbook provides excellent discussions around these topics, so please consult it.

Build a linear model to estimate the relationship between the log

of wage (lwage) and education

(educ).

log_wage_model <- lm(lwage ~ educ, data = wage1)Print the summary of the results.

summary(log_wage_model)| Dependent variable: | |

| lwage | |

| educ | 0.08274*** (0.00757) |

| Constant | 0.58377*** (0.09734) |

| Observations | 526 |

| R2 | 0.18581 |

| Adjusted R2 | 0.18425 |

| Residual Std. Error | 0.48008 (df = 524) |

| F Statistic | 119.58160*** (df = 1; 524) |

| Note: | p<0.1; p<0.05; p<0.01 |

Plot the

wage

vs educ. The blue line represents the least squares

fit.

Chapter 3: Multiple Regression Analysis: Estimation

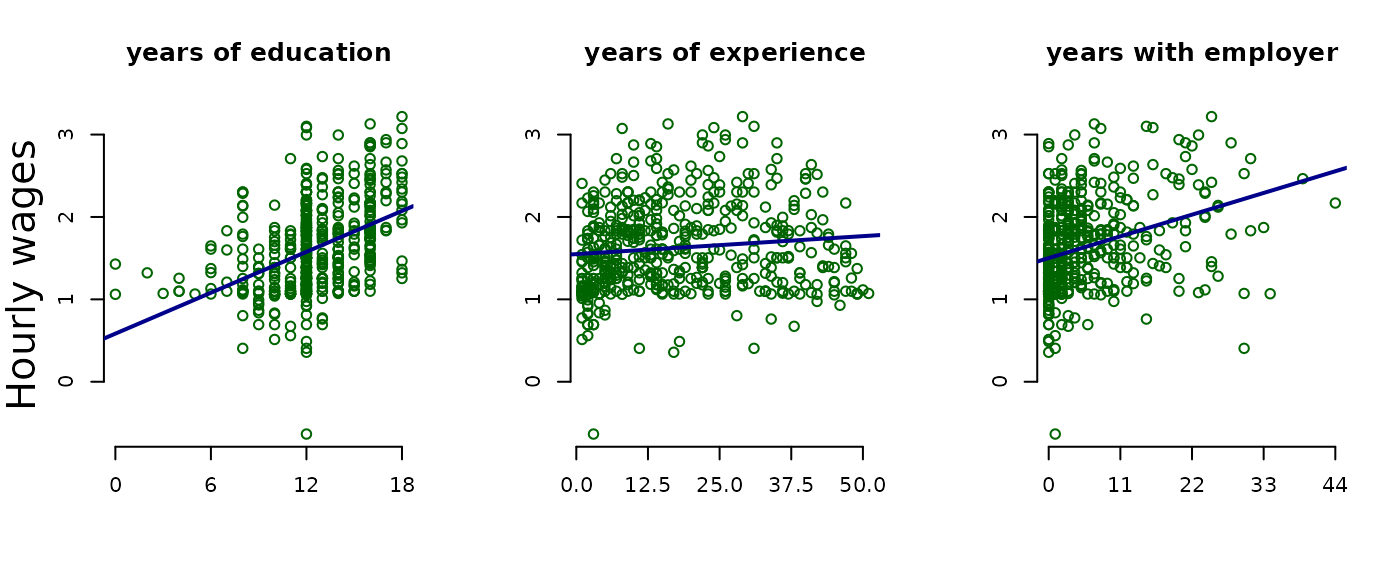

Example 3.2: Hourly Wage Equation

Check the documentation for variable information

?wage1: log of the average hourly earnings

: years of education

: years of potential experience

: years with current employer

Plot the variables against lwage and compare their

distributions and slope

()

of the simple regression lines.

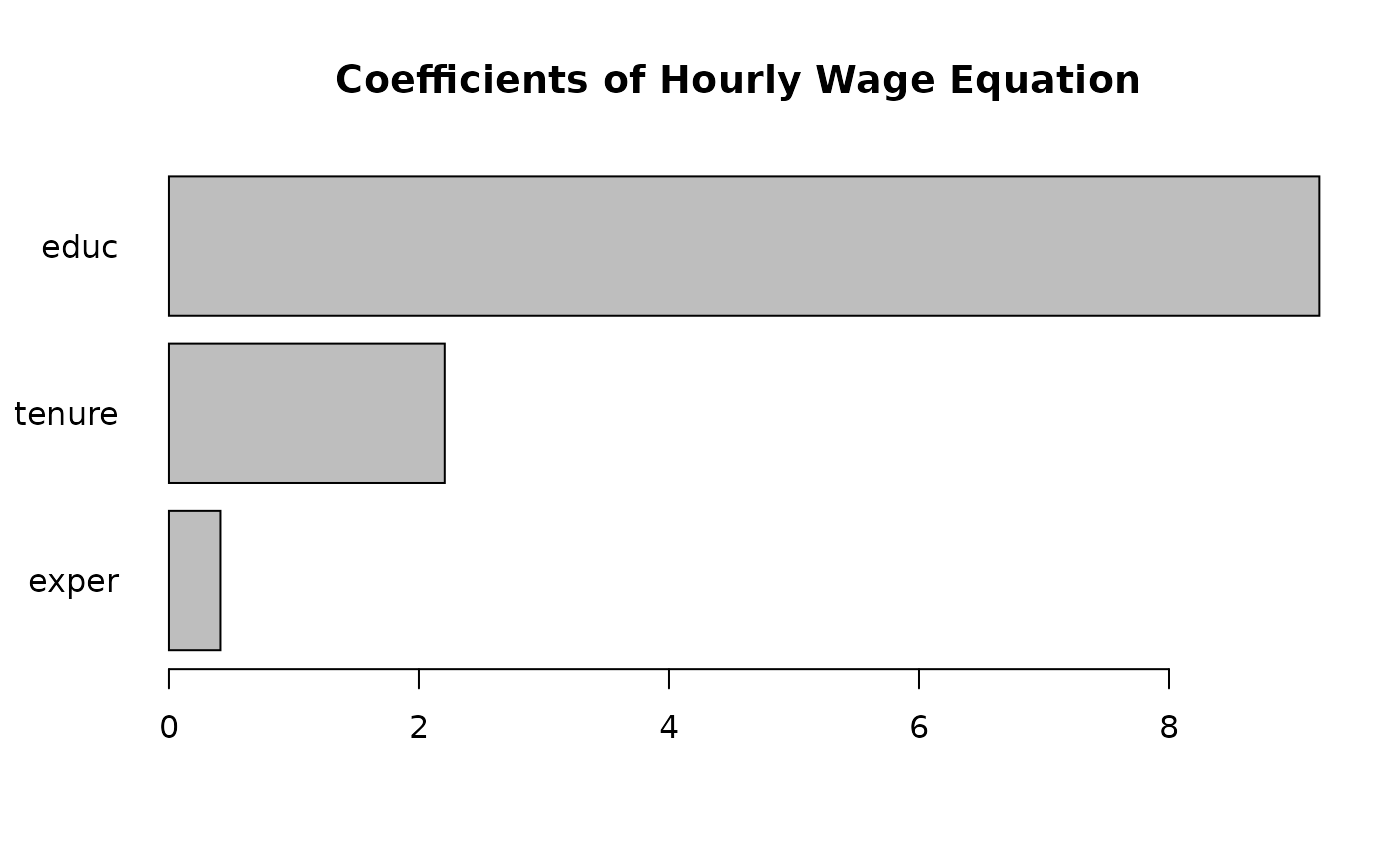

Estimate the model regressing educ, exper, and tenure against log(wage).

hourly_wage_model <- lm(lwage ~ educ + exper + tenure, data = wage1)Print the estimated model coefficients:

coefficients(hourly_wage_model)| Coefficients | |

|---|---|

| (Intercept) | 0.2844 |

| educ | 0.0920 |

| exper | 0.0041 |

| tenure | 0.0221 |

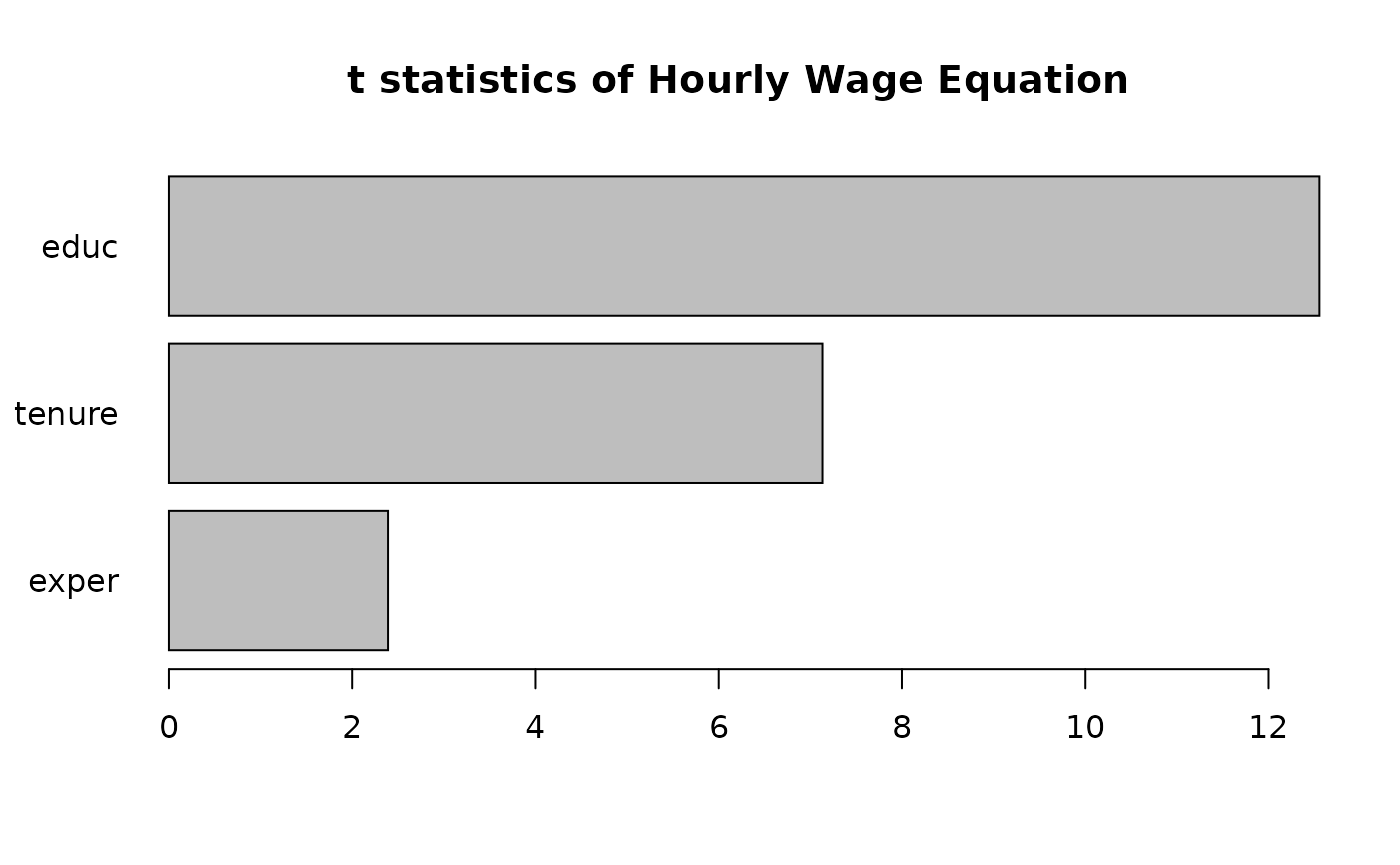

Plot the coefficients, representing percentage impact of each

variable on

wage

for a quick comparison.

Chapter 4: Multiple Regression Analysis: Inference

Example 4.1 Hourly Wage Equation

Using the same model estimated in

example: 3.2, examine and compare the

standard errors associated with each coefficient. Like the textbook,

these are contained in parenthesis next to each associated

coefficient.

summary(hourly_wage_model)| Dependent variable: | |

| lwage | |

| educ | 0.09203*** (0.00733) |

| exper | 0.00412** (0.00172) |

| tenure | 0.02207*** (0.00309) |

| Constant | 0.28436*** (0.10419) |

| Observations | 526 |

| R2 | 0.31601 |

| Adjusted R2 | 0.31208 |

| Residual Std. Error | 0.44086 (df = 522) |

| F Statistic | 80.39092*** (df = 3; 522) |

| Note: | p<0.1; p<0.05; p<0.01 |

For the years of experience variable, or exper, use

coefficient and Standard Error to compute the

statistic:

Fortunately, R includes

statistics in the summary of model diagnostics.

summary(hourly_wage_model)$coefficients| Estimate | Std. Error | t value | Pr(>|t|) | |

|---|---|---|---|---|

| (Intercept) | 0.28436 | 0.10419 | 2.72923 | 0.00656 |

| educ | 0.09203 | 0.00733 | 12.55525 | 0.00000 |

| exper | 0.00412 | 0.00172 | 2.39144 | 0.01714 |

| tenure | 0.02207 | 0.00309 | 7.13307 | 0.00000 |

Plot the statistics for a visual comparison:

Example 4.7 Effect of Job Training on Firm

Scrap Rates

Load the jtrain data set.

data("jtrain")

?jtrainFrom H. Holzer, R. Block, M. Cheatham, and J. Knott (1993), Are Training Subsidies Effective? The Michigan Experience, Industrial and Labor Relations Review 46, 625-636. The authors kindly provided the data.

1987, 1988, or 1989

=1 if unionized

Log(scrap rate per 100 items)

(total hours training) / (total employees trained)

Log(annual sales, $)

Log(umber of employees at plant)

First, use the subset function and it’s argument by the

same name to return observations which occurred in 1987

and are not union. At the same time, use the

select argument to return only the variables of interest

for this problem.

jtrain_subset <- subset(jtrain, subset = (year == 1987 & union == 0),

select = c(year, union, lscrap, hrsemp, lsales, lemploy))Next, test for missing values. One can “eyeball” these with R

Studio’s View function, but a more precise approach

combines the sum and is.na functions to return

the total number of observations equal to NA.

## [1] 156While R’s lm function will automatically

remove missing NA values, eliminating these manually will

produce more clearly proportioned graphs for exploratory analysis. Call

the na.omit function to remove all missing values and

assign the new data.frame object the name

jtrain_clean.

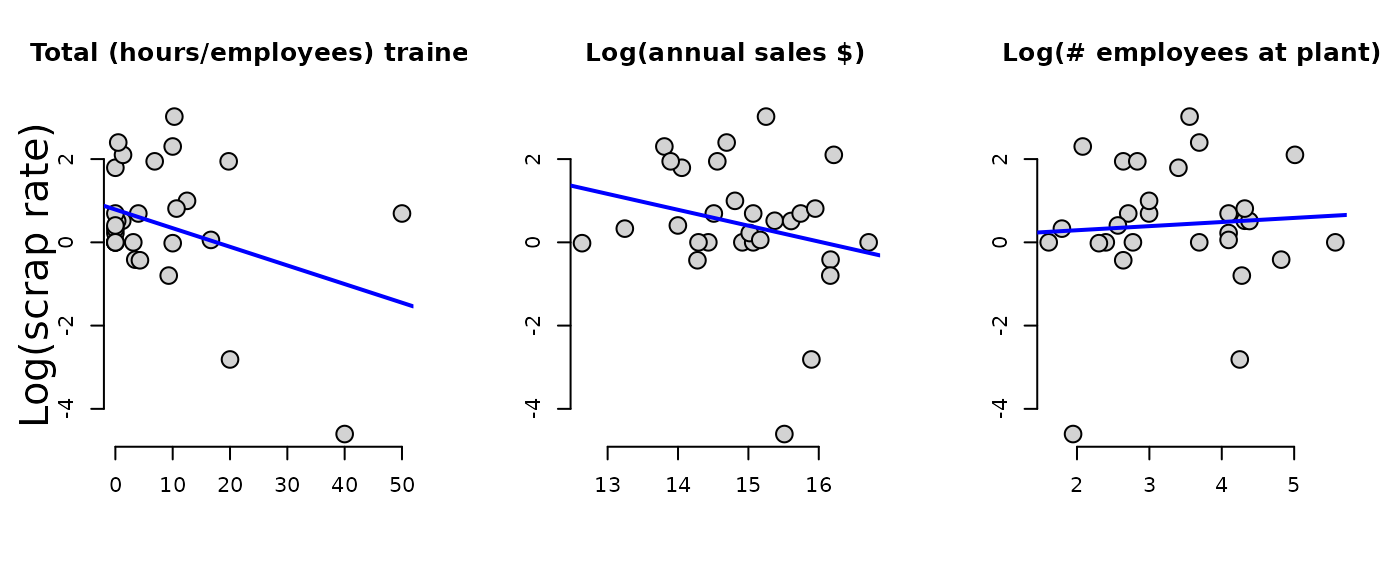

jtrain_clean <- na.omit(jtrain_subset)Use jtrain_clean to plot the variables of interest

against lscrap. Visually observe the respective

distributions for each variable, and compare the slope

()

of the simple regression lines.

Now create the linear model regressing hrsemp(total

hours training/total employees trained), lsales(log of

annual sales), and lemploy(the log of the number of the

employees), against lscrap(the log of the scrape rate).

linear_model <- lm(lscrap ~ hrsemp + lsales + lemploy, data = jtrain_clean)Finally, print the complete summary diagnostics of the model.

summary(linear_model)| Dependent variable: | |

| lscrap | |

| hrsemp | -0.02927 (0.02280) |

| lsales | -0.96203** (0.45252) |

| lemploy | 0.76147* (0.40743) |

| Constant | 12.45837** (5.68677) |

| Observations | 29 |

| R2 | 0.26243 |

| Adjusted R2 | 0.17392 |

| Residual Std. Error | 1.37604 (df = 25) |

| F Statistic | 2.96504* (df = 3; 25) |

| Note: | p<0.1; p<0.05; p<0.01 |

Chapter 5: Multiple Regression Analysis: OLS Asymptotics

Example 5.1: Housing Prices and Distance From

an Incinerator

Load the hprice3 data set.

data("hprice3")Log(selling price)

Log(distance from house to incinerator, feet)

Log(square footage of house)

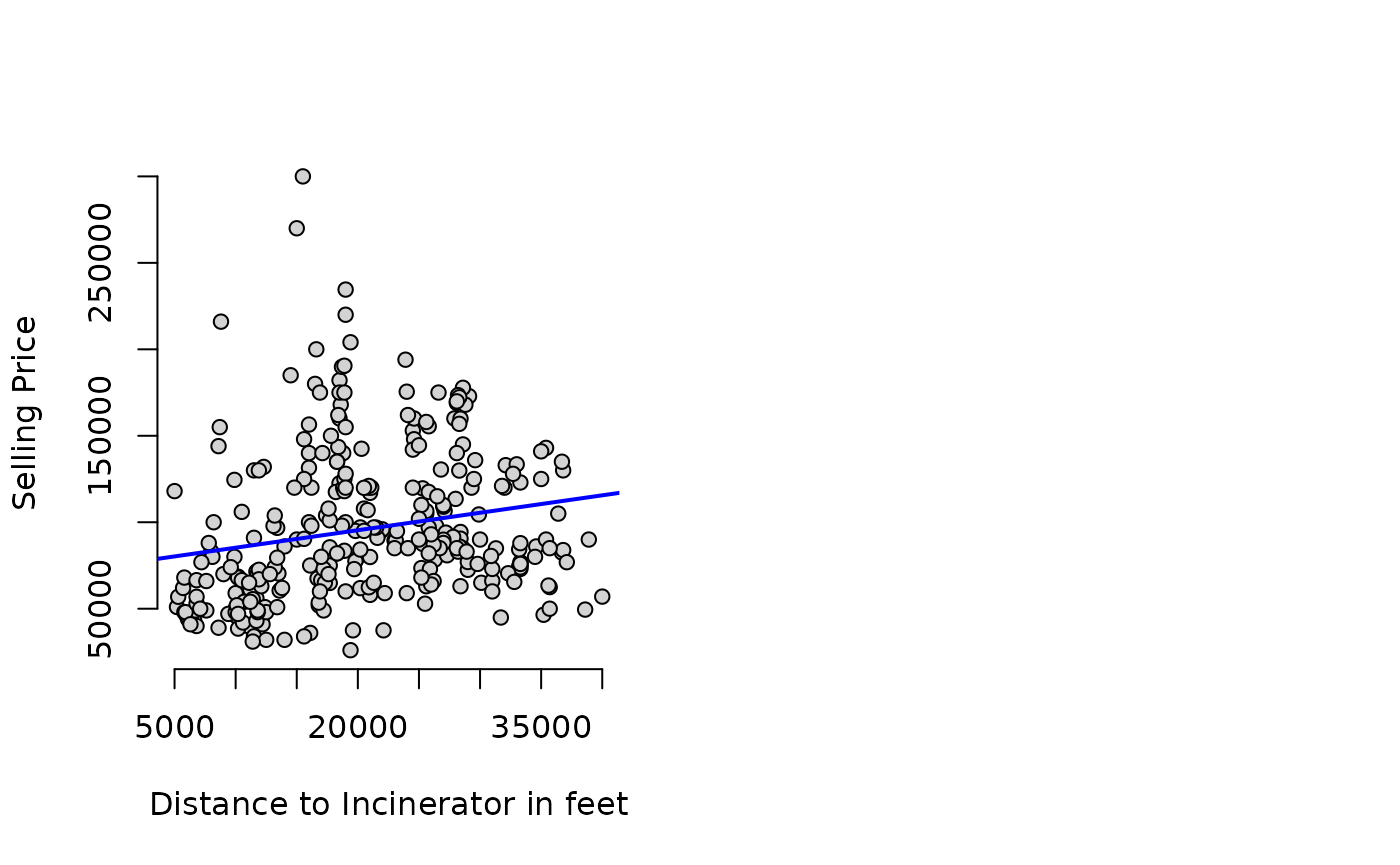

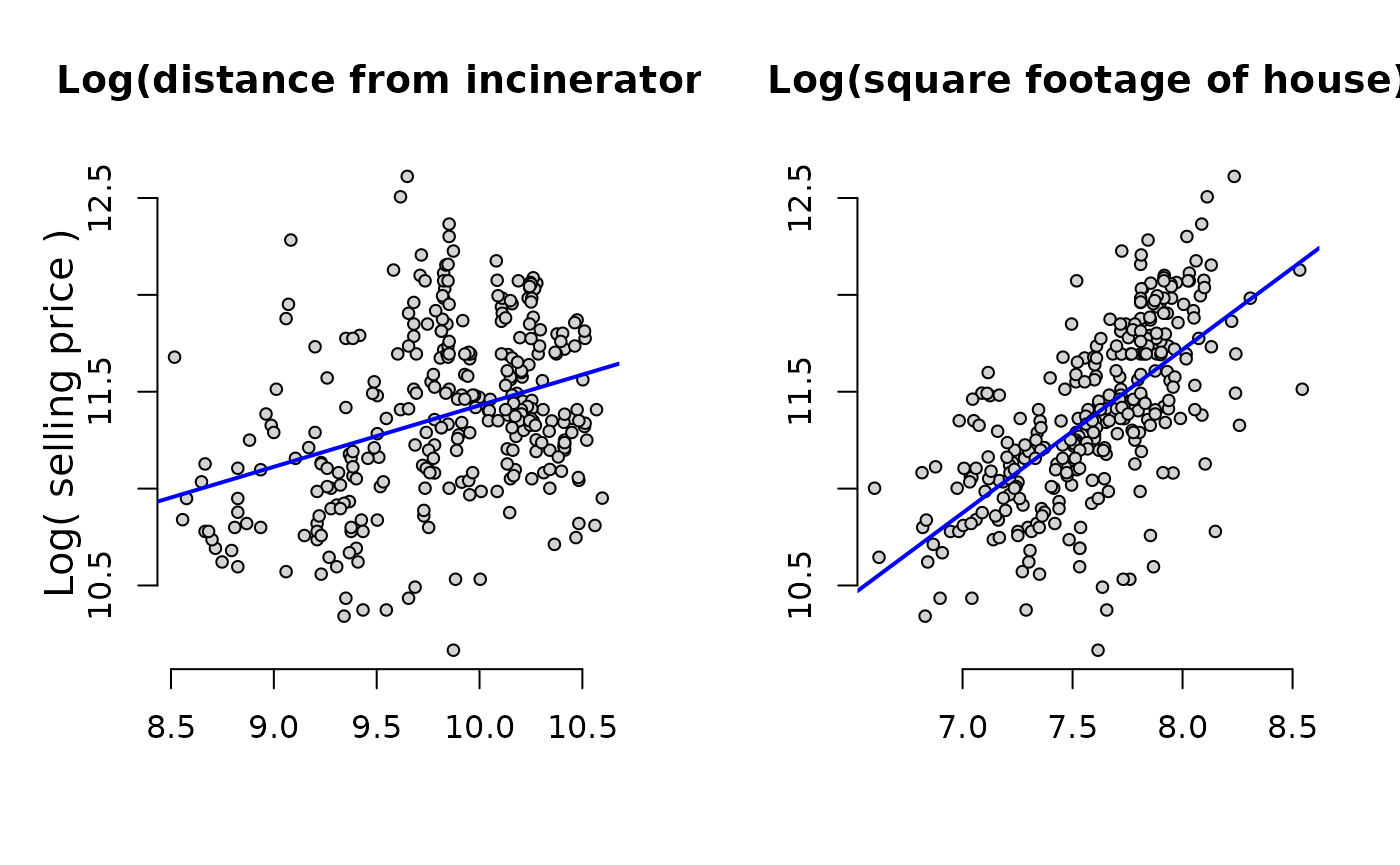

Graph the prices of housing against distance from an incinerator:

Next, model the

price

against the

dist

to estimate the percentage relationship between the two.

price_dist_model <- lm(lprice ~ ldist, data = hprice3)Create another model that controls for “quality” variables, such as

square footage area per house.

price_area_model <- lm(lprice ~ ldist + larea, data = hprice3)Compare the coefficients of both models. Notice that adding

area improves the quality of the model, but also reduces

the coefficient size of dist.

| Dependent variable: | ||

| lprice | ||

| (1) | (2) | |

| ldist | 0.31722*** (0.04811) | 0.19623*** (0.03816) |

| larea | 0.78368*** (0.05358) | |

| Constant | 8.25750*** (0.47383) | 3.49394*** (0.49065) |

| Observations | 321 | 321 |

| R2 | 0.11994 | 0.47385 |

| Adjusted R2 | 0.11718 | 0.47054 |

| Residual Std. Error | 0.41170 (df = 319) | 0.31883 (df = 318) |

| F Statistic | 43.47673*** (df = 1; 319) | 143.19470*** (df = 2; 318) |

| Note: | p<0.1; p<0.05; p<0.01 | |

Graphing illustrates the larger coefficient for

area.

Chapter 6: Multiple Regression: Further Issues

Example 6.1: Effects of Pollution on Housing

Prices, standardized.

Load the hprice2 data and view the documentation.

data("hprice2")

?hprice2Data from Hedonic Housing Prices and the Demand for Clean Air, by Harrison, D. and D.L.Rubinfeld, Journal of Environmental Economics and Management 5, 81-102. Diego Garcia, a former Ph.D. student in economics at MIT, kindly provided these data, which he obtained from the book Regression Diagnostics: Identifying Influential Data and Sources of Collinearity, by D.A. Belsey, E. Kuh, and R. Welsch, 1990. New York: Wiley.

: median housing price.

: Nitrous Oxide concentration; parts per million.

: number of reported crimes per capita.

: average number of rooms in houses in the community.

: weighted distance of the community to 5 employment centers.

: average student-teacher ratio of schools in the community.

Estimate the usual lm model.

housing_level <- lm(price ~ nox + crime + rooms + dist + stratio, data = hprice2)Estimate the same model, but standardized coefficients by wrapping

each variable with R’s scale function:

housing_standardized <- lm(scale(price) ~ 0 + scale(nox) + scale(crime) + scale(rooms) + scale(dist) + scale(stratio), data = hprice2)Compare results, and observe

| Dependent variable: | ||

| price | scale(price) | |

| (1) | (2) | |

| nox | -2,706.43300*** (354.08690) | |

| crime | -153.60100*** (32.92883) | |

| rooms | 6,735.49800*** (393.60370) | |

| dist | -1,026.80600*** (188.10790) | |

| stratio | -1,149.20400*** (127.42870) | |

| scale(nox) | -0.34045*** (0.04450) | |

| scale(crime) | -0.14328*** (0.03069) | |

| scale(rooms) | 0.51389*** (0.03000) | |

| scale(dist) | -0.23484*** (0.04298) | |

| scale(stratio) | -0.27028*** (0.02994) | |

| Constant | 20,871.13000*** (5,054.59900) | |

| Observations | 506 | 506 |

| R2 | 0.63567 | 0.63567 |

| Adjusted R2 | 0.63202 | 0.63203 |

| Residual Std. Error | 5,586.19800 (df = 500) | 0.60601 (df = 501) |

| F Statistic | 174.47330*** (df = 5; 500) | 174.82220*** (df = 5; 501) |

| Note: | p<0.1; p<0.05; p<0.01 | |

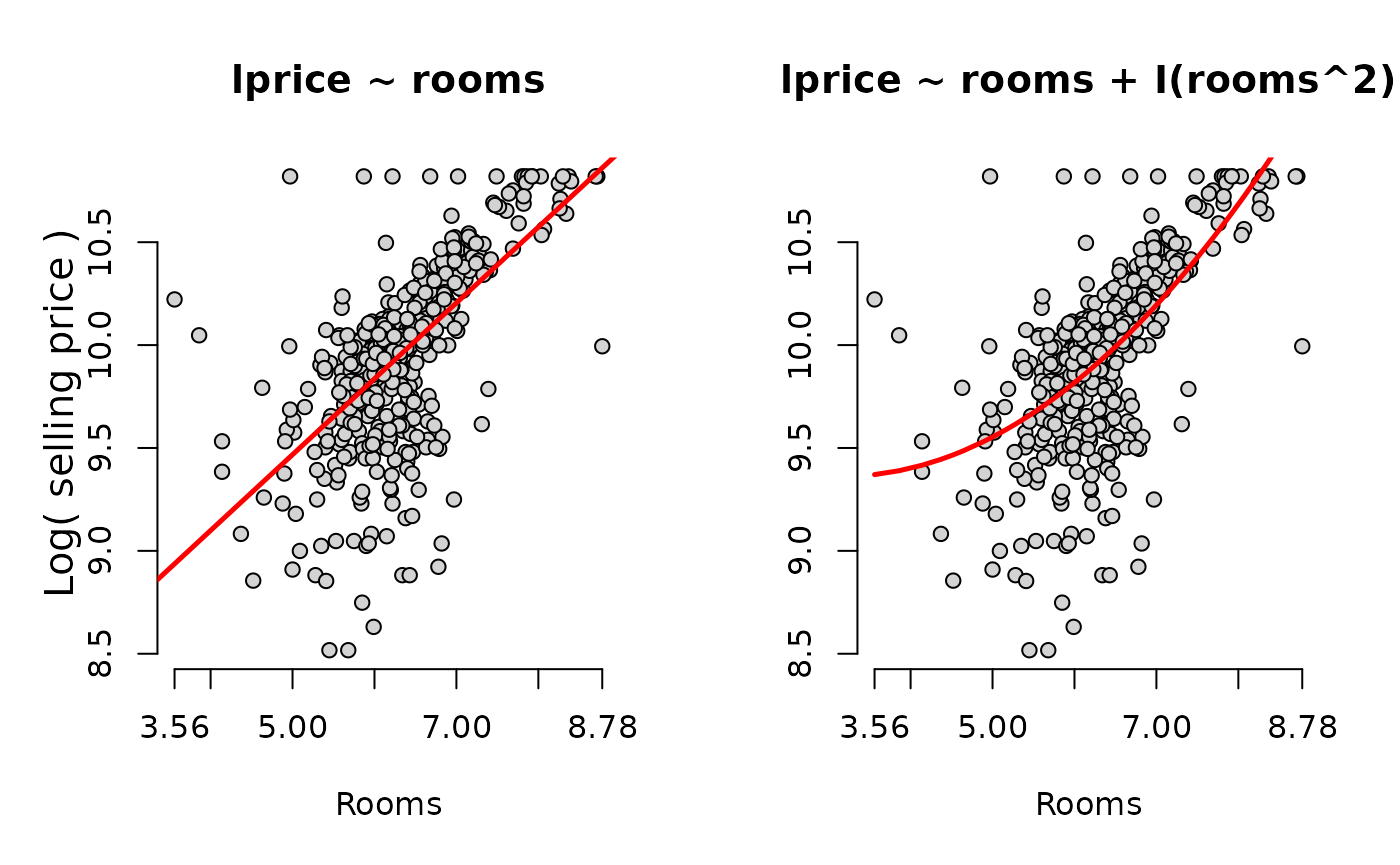

Example 6.2: Effects of Pollution on Housing

Prices, Quadratic Interactive Term

Modify the housing model from

example 4.5, adding a quadratic term in

rooms:

housing_model_4.5 <- lm(lprice ~ lnox + log(dist) + rooms + stratio, data = hprice2)

housing_model_6.2 <- lm(lprice ~ lnox + log(dist) + rooms + I(rooms^2) + stratio,

data = hprice2)Compare the results with the model from example 6.1.

| Dependent variable: | ||

| lprice | ||

| (1) | (2) | |

| lnox | -0.95354*** (0.11674) | -0.90168*** (0.11469) |

| log(dist) | -0.13434*** (0.04310) | -0.08678** (0.04328) |

| rooms | 0.25453*** (0.01853) | -0.54511*** (0.16545) |

| I(rooms2) | 0.06226*** (0.01280) | |

| stratio | -0.05245*** (0.00590) | -0.04759*** (0.00585) |

| Constant | 11.08386*** (0.31811) | 13.38548*** (0.56647) |

| Observations | 506 | 506 |

| R2 | 0.58403 | 0.60281 |

| Adjusted R2 | 0.58071 | 0.59884 |

| Residual Std. Error | 0.26500 (df = 501) | 0.25921 (df = 500) |

| F Statistic | 175.85520*** (df = 4; 501) | 151.77040*** (df = 5; 500) |

| Note: | p<0.1; p<0.05; p<0.01 | |

Estimate the minimum turning point at which the rooms

interactive term changes from negative to positive.

beta_1 <- summary(housing_model_6.2)$coefficients["rooms",1]

beta_2 <- summary(housing_model_6.2)$coefficients["I(rooms^2)",1]

turning_point <- abs(beta_1 / (2*beta_2))

print(turning_point)## [1] 4.37763Compute the percent change across a range of average rooms. Include the smallest, turning point, and largest.

Rooms <- c(min(hprice2$rooms), 4, turning_point, 5, 5.5, 6.45, 7.5, max(hprice2$rooms))

Percent.Change <- 100*(beta_1 + 2*beta_2*Rooms)

kable(data.frame(Rooms, Percent.Change))| Rooms | Percent.Change |

|---|---|

| 3.56000 | -10.181324 |

| 4.00000 | -4.702338 |

| 4.37763 | 0.000000 |

| 5.00000 | 7.749903 |

| 5.50000 | 13.976023 |

| 6.45000 | 25.805651 |

| 7.50000 | 38.880503 |

| 8.78000 | 54.819367 |

Graph the log of the selling price against the number of rooms. Superimpose a simple model as well as a quadratic model and examine the difference.

Chapter 7: Multiple Regression Analysis with Qualitative Information

Example 7.4: Housing Price Regression,

Qualitative Binary variable

This time, use the hrprice1 data.

data("hprice1")

?hprice1Data collected from the real estate pages of the Boston Globe during 1990. These are homes that sold in the Boston, MA area.

Log(house price, $1000s)

Log(size of lot in square feet)

Log(size of house in square feet)

number of bdrms

=1 if home is colonial style

Estimate the coefficients of the above linear model on the

hprice data set.

housing_qualitative <- lm(lprice ~ llotsize + lsqrft + bdrms + colonial, data = hprice1)

summary(housing_qualitative)| Dependent variable: | |

| lprice | |

| llotsize | 0.16782*** (0.03818) |

| lsqrft | 0.70719*** (0.09280) |

| bdrms | 0.02683 (0.02872) |

| colonial | 0.05380 (0.04477) |

| Constant | -1.34959** (0.65104) |

| Observations | 88 |

| R2 | 0.64907 |

| Adjusted R2 | 0.63216 |

| Residual Std. Error | 0.18412 (df = 83) |

| F Statistic | 38.37846*** (df = 4; 83) |

| Note: | p<0.1; p<0.05; p<0.01 |

Chapter 8: Heteroskedasticity

Example 8.9: Determinants of Personal Computer

Ownership

Christopher Lemmon, a former MSU undergraduate, collected these data

from a survey he took of MSU students in Fall 1994. Load

gpa1 and create a new variable combining the

fathcoll and mothcoll, into

parcoll. This new column indicates if either parent went to

college.

data("gpa1")

gpa1$parcoll <- as.integer(gpa1$fathcoll==1 | gpa1$mothcoll)

GPA_OLS <- lm(PC ~ hsGPA + ACT + parcoll, data = gpa1)Calculate the weights and then pass them to the weights

argument.

weights <- GPA_OLS$fitted.values * (1-GPA_OLS$fitted.values)

GPA_WLS <- lm(PC ~ hsGPA + ACT + parcoll, data = gpa1, weights = 1/weights)Compare the OLS and WLS model in the table below:

| Dependent variable: | ||

| PC | ||

| (1) | (2) | |

| hsGPA | 0.06539 (0.13726) | 0.03270 (0.12988) |

| ACT | 0.00056 (0.01550) | 0.00427 (0.01545) |

| parcoll | 0.22105** (0.09296) | 0.21519** (0.08629) |

| Constant | -0.00043 (0.49054) | 0.02621 (0.47665) |

| Observations | 141 | 141 |

| R2 | 0.04153 | 0.04644 |

| Adjusted R2 | 0.02054 | 0.02556 |

| Residual Std. Error (df = 137) | 0.48599 | 1.01624 |

| F Statistic (df = 3; 137) | 1.97851 | 2.22404* |

| Note: | p<0.1; p<0.05; p<0.01 | |

Chapter 9: More on Specification and Data Issues

Example 9.8: R&D Intensity and Firm

Size

From Businessweek R&D Scoreboard, October 25, 1991. Load the data and estimate the model.

Plotting the data reveals the outlier on the far right of the plot, which will skew the results of our model.

So, we can estimate the model without that data point to gain a

better understanding of how sales and profmarg

describe rdintens for most firms. We can use the

subset argument of the linear model function to indicate

that we only want to estimate the model using data that is less than the

highest sales.

The table below compares the results of both models side by side. By removing the outlier firm, become a more significant determination of R&D expenditures.

| Dependent variable: | ||

| rdintens | ||

| (1) | (2) | |

| sales | 0.00005 (0.00004) | 0.00019** (0.00008) |

| profmarg | 0.04462 (0.04618) | 0.04784 (0.04448) |

| Constant | 2.62526*** (0.58553) | 2.29685*** (0.59180) |

| Observations | 32 | 31 |

| R2 | 0.07612 | 0.17281 |

| Adjusted R2 | 0.01240 | 0.11372 |

| Residual Std. Error | 1.86205 (df = 29) | 1.79218 (df = 28) |

| F Statistic | 1.19465 (df = 2; 29) | 2.92476* (df = 2; 28) |

| Note: | p<0.1; p<0.05; p<0.01 | |

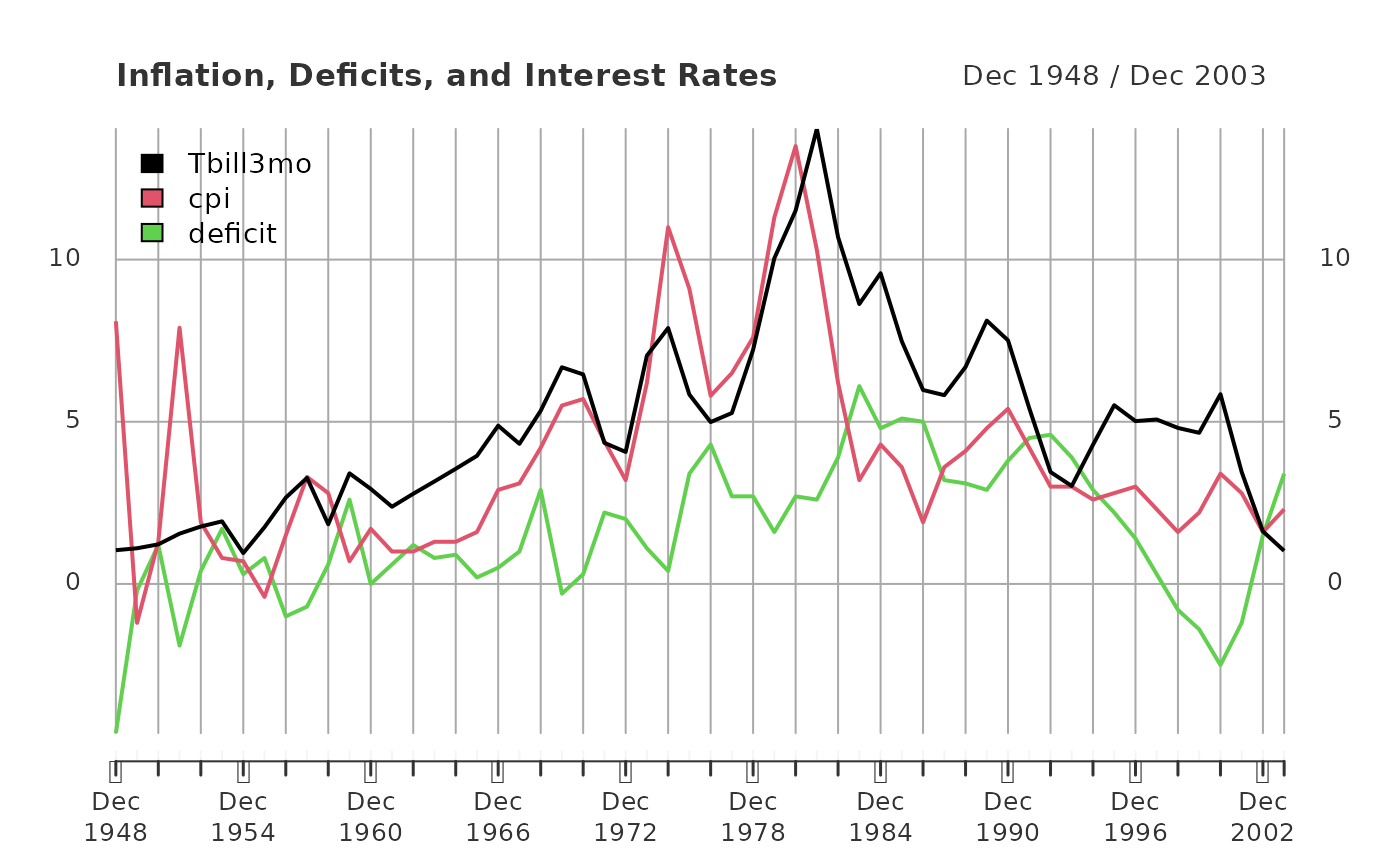

Chapter 10: Basic Regression Analysis with Time Series Data

Example 10.2: Effects of Inflation and Deficits

on Interest Rates

Data from the Economic Report of the President, 2004, Tables B-64, B-73, and B-79.

data("intdef") # load data

# load eXtensible Time Series package.

# xts is excellent for time series plots and

# properly indexing time series.

library(xts)

# create xts object from data.frame

# First, index year as yearmon class of monthly data.

# Note: I add 11/12 to set the month to December, end of year.

index <- zoo::as.yearmon(intdef$year + 11/12)

# Next, create the xts object, ordering by the index above.

intdef.xts <- xts(intdef[ ,-1], order.by = index)

# extract 3-month Tbill, inflation, and deficit data

intdef.xts <- intdef.xts[ ,c("i3", "inf", "def")]

# rename with clearer names

colnames(intdef.xts) <- c("Tbill3mo", "cpi", "deficit")

# plot the object, add a title, and place legend at top left.

plot(x = intdef.xts,

main = "Inflation, Deficits, and Interest Rates",

legend.loc = "topleft")

# Run a Linear regression model

tbill_model <- lm(Tbill3mo ~ cpi + deficit, data = intdef.xts)| Dependent variable: | |

| Tbill3mo | |

| cpi | 0.60587*** (0.08213) |

| deficit | 0.51306*** (0.11838) |

| Constant | 1.73327*** (0.43197) |

| Observations | 56 |

| R2 | 0.60207 |

| Adjusted R2 | 0.58705 |

| Residual Std. Error | 1.84316 (df = 53) |

| F Statistic | 40.09424*** (df = 2; 53) |

| Note: | p<0.1; p<0.05; p<0.01 |

Now lets update the example with current data, pull from the Federal Reserve Economic Research (FRED) using the quantmod package. Other than the convenient API, the package also formats time series data into xts: eXtensible Time Series objects, which add many feature and benefits when working with time series.

# DO NOT RUN

library(quantmod)

# Tbill, 3 month

getSymbols("TB3MS", src = "FRED")

# convert to annual observations and convert index to type `yearmon`.

TB3MS <- to.yearly(TB3MS, OHLC=FALSE, drop.time = TRUE)

index(TB3MS) <- zoo::as.yearmon(index(TB3MS))

# Inflation

getSymbols("FPCPITOTLZGUSA", src = "FRED")

# Convert the index to yearmon and shift FRED's Jan 1st to Dec

index(FPCPITOTLZGUSA) <- zoo::as.yearmon(index(FPCPITOTLZGUSA)) + 11/12

# Rename and update column names

inflation <- FPCPITOTLZGUSA

colnames(inflation) <- "inflation"

## Deficit, percent of GDP: Federal outlays - federal receipts

# Download outlays

getSymbols("FYFRGDA188S", src = "FRED")

# Lets move the index from Jan 1st to Dec 30th/31st

index(FYFRGDA188S) <- zoo::as.yearmon(index(FYFRGDA188S)) + 11/12

# Rename and update column names

outlays <- FYFRGDA188S

colnames(outlays) <- "outlays"

# Download receipts

getSymbols("FYONGDA188S", src = "FRED")

# Lets move the index from Jan 1st to Dec 30th/31st

index(FYONGDA188S) <- zoo::as.yearmon(index(FYONGDA188S)) + 11/12

# Rename and update column names

receipts <- FYONGDA188S

colnames(receipts) <- "receipts"Now that all data has been downloaded, we can calculate the deficit

from the federal outlays and receipts data.

Next, we will merge our new deficit variable with

inflation and TB3MS variables. As these are

all xts times series objects, the merge

function will automatically key off each series time date index,

insuring integrity and alignment among each observation and its

respective date. Additionally, xts provides easy chart construction with

its plot method.

# DO NOT RUN

# create deficits from outlays - receipts

# xts objects respect their indexing and outline the future

deficit <- outlays - receipts

colnames(deficit) <- "deficit"

# Merge and remove leading and trailing NAs for a balanced data matrix

intdef_updated <- merge(TB3MS, inflation, deficit)

intdef_updated <- zoo::na.trim(intdef_updated)

#Plot all

plot(intdef_updated,

main = "T-bill (3mo rate), inflation, and deficit (% of GDP)",

legend.loc = "topright",)Now lets run the model again. Inflation plays a much more prominent role in the 3 month T-bill rate, than the deficit.

# DO NOT RUN

updated_model <- lm(TB3MS ~ inflation + deficit, data = intdef_updated)Chapter 11: Further Issues in Using OLS with with Time Series Data

Example 11.7: Wages and

Productivity

Data from the Economic Report of the President, 1989, Table B-47. The data are for the non-farm business sector.

| Dependent variable: | ||

| lhrwage | diff(lhrwage) | |

| (1) | (2) | |

| loutphr | 1.63964*** (0.09335) | |

| t | -0.01823*** (0.00175) | |

| diff(loutphr) | 0.80932*** (0.17345) | |

| Constant | -5.32845*** (0.37445) | -0.00366 (0.00422) |

| Observations | 41 | 40 |

| R2 | 0.97122 | 0.36424 |

| Adjusted R2 | 0.96971 | 0.34750 |

| Residual Std. Error (df = 38) | 0.02854 | 0.01695 |

| F Statistic | 641.22430*** (df = 2; 38) | 21.77054*** (df = 1; 38) |

| Note: | p<0.1; p<0.05; p<0.01 | |

Chapter 12: Serial Correlation and Heteroskedasticiy in Time Series Regressions

Example 12.8: Heteroskedasticity and the

Efficient Markets Hypothesis

These are Wednesday closing prices of value-weighted NYSE average, available in many publications. Wooldridge does not recall the particular source used when he collected these data at MIT, but notes probably the easiest way to get similar data is to go to the NYSE web site, www.nyse.com.

data("nyse")

?nyse

return_AR1 <-lm(return ~ return_1, data = nyse)

return_mu <- residuals(return_AR1)

mu2_hat_model <- lm(return_mu^2 ~ return_1, data = return_AR1$model)| Dependent variable: | ||

| return | return_mu2 | |

| (1) | (2) | |

| return_1 | 0.05890 (0.03802) | -1.10413*** (0.20140) |

| Constant | 0.17963** (0.08074) | 4.65650*** (0.42768) |

| Observations | 689 | 689 |

| R2 | 0.00348 | 0.04191 |

| Adjusted R2 | 0.00203 | 0.04052 |

| Residual Std. Error (df = 687) | 2.11040 | 11.17847 |

| F Statistic (df = 1; 687) | 2.39946 | 30.05460*** |

| Note: | p<0.1; p<0.05; p<0.01 | |

Example 12.9: ARCH in Stock

Returns

We still have return_mu in the working environment so we

can use it to create

,

(mu2_hat) and

(mu2_hat_1). Notice the use R’s matrix subset

operations to perform the lag operation. We drop the first observation

of mu2_hat and squared the results. Next, we remove the

last observation of mu2_hat_1 using the subtraction

operator combined with a call to the NROW function on

return_mu. Now, both contain

observations and we can estimate a standard linear model.

mu2_hat <- return_mu[-1]^2

mu2_hat_1 <- return_mu[-NROW(return_mu)]^2

arch_model <- lm(mu2_hat ~ mu2_hat_1)| Dependent variable: | |

| mu2_hat | |

| mu2_hat_1 | 0.33706*** (0.03595) |

| Constant | 2.94743*** (0.44023) |

| Observations | 688 |

| R2 | 0.11361 |

| Adjusted R2 | 0.11231 |

| Residual Std. Error | 10.75907 (df = 686) |

| F Statistic | 87.92263*** (df = 1; 686) |

| Note: | p<0.1; p<0.05; p<0.01 |

Chapter 13: Pooling Cross Sections across Time: Simple Panel Data Methods

Example 13.7: Effect of Drunk Driving Laws on

Traffic Fatalities

Wooldridge collected these data from two sources, the 1992 Statistical Abstract of the United States (Tables 1009, 1012) and A Digest of State Alcohol-Highway Safety Related Legislation, 1985 and 1990, published by the U.S. National Highway Traffic Safety Administration.

data("traffic1")

?traffic1

DD_model <- lm(cdthrte ~ copen + cadmn, data = traffic1)| Dependent variable: | |

| cdthrte | |

| copen | -0.41968** (0.20559) |

| cadmn | -0.15060 (0.11682) |

| Constant | -0.49679*** (0.05243) |

| Observations | 51 |

| R2 | 0.11867 |

| Adjusted R2 | 0.08194 |

| Residual Std. Error | 0.34350 (df = 48) |

| F Statistic | 3.23144** (df = 2; 48) |

| Note: | p<0.1; p<0.05; p<0.01 |

Chapter 18: Advanced Time Series Topics

Example 18.8: FORECASTING THE U.S. UNEMPLOYMENT

RATE

Data from Economic Report of the President, 2004, Tables B-42 and B-64.

data("phillips")

?phillipsEstimate the linear model in the usual way and note the use of the

subset argument to define data equal to and before the year

1996.

phillips_train <- subset(phillips, year <= 1996)

unem_AR1 <- lm(unem ~ unem_1, data = phillips_train)

unem_inf_VAR1 <- lm(unem ~ unem_1 + inf_1, data = phillips_train)| Dependent variable: | ||

| unem | ||

| (1) | (2) | |

| unem_1 | 0.73235*** (0.09689) | 0.64703*** (0.08381) |

| inf_1 | 0.18358*** (0.04118) | |

| Constant | 1.57174*** (0.57712) | 1.30380** (0.48969) |

| Observations | 48 | 48 |

| R2 | 0.55397 | 0.69059 |

| Adjusted R2 | 0.54427 | 0.67684 |

| Residual Std. Error | 1.04857 (df = 46) | 0.88298 (df = 45) |

| F Statistic | 57.13184*** (df = 1; 46) | 50.21941*** (df = 2; 45) |

| Note: | p<0.1; p<0.05; p<0.01 | |

Now, use the subset argument to create our testing data

set containing observation after 1996. Next, pass the both the model

object and the test set to the predict function for both

models. Finally, cbind or “column bind” both forecasts as

well as the year and unemployment rate of the test set.

phillips_test <- subset(phillips, year >= 1997)

AR1_forecast <- predict.lm(unem_AR1, newdata = phillips_test)

VAR1_forecast <- predict.lm(unem_inf_VAR1, newdata = phillips_test)

kable(cbind(phillips_test[ ,c("year", "unem")], AR1_forecast, VAR1_forecast))| year | unem | AR1_forecast | VAR1_forecast | |

|---|---|---|---|---|

| 50 | 1997 | 4.9 | 5.526452 | 5.348468 |

| 51 | 1998 | 4.5 | 5.160275 | 4.896451 |

| 52 | 1999 | 4.2 | 4.867333 | 4.509137 |

| 53 | 2000 | 4.0 | 4.647627 | 4.425175 |

| 54 | 2001 | 4.8 | 4.501157 | 4.516062 |

| 55 | 2002 | 5.8 | 5.087040 | 4.923537 |

| 56 | 2003 | 6.0 | 5.819394 | 5.350271 |

Appendix

Using R for Introductory Econometrics

This is an excellent open source complimentary text to “Introductory Econometrics” by Jeffrey M. Wooldridge and should be your number one resource. This excerpt from the book’s website:

This book introduces the popular, powerful and free programming language and software package R with a focus on the implementation of standard tools and methods used in econometrics. Unlike other books on similar topics, it does not attempt to provide a self-contained discussion of econometric models and methods. Instead, it builds on the excellent and popular textbook “Introductory Econometrics” by Jeffrey M. Wooldridge.

Heiss, Florian. Using R for Introductory Econometrics. ISBN: 979-8648424364, CreateSpace Independent Publishing Platform, 2020, Dusseldorf, Germany.

Applied Econometrics with R

From the publisher’s website:

This is the first book on applied econometrics using the R system for statistical computing and graphics. It presents hands-on examples for a wide range of econometric models, from classical linear regression models for cross-section, time series or panel data and the common non-linear models of microeconometrics such as logit, probit and tobit models, to recent semiparametric extensions. In addition, it provides a chapter on programming, including simulations, optimization, and an introduction to R tools enabling reproducible econometric research. An R package accompanying this book, AER, is available from the Comprehensive R Archive Network (CRAN) at https://CRAN.R-project.org/package=AER.

Kleiber, Christian and Achim Zeileis. Applied Econometrics with R. ISBN 978-0-387-77316-2, Springer-Verlag, 2008, New York. https://link.springer.com/book/10.1007/978-0-387-77318-6

Bibliography

Jeffrey M. Wooldridge (2020). Introductory Econometrics: A Modern Approach, 7th edition. ISBN-13: 978-1-337-55886-0. Mason, Ohio :South-Western Cengage Learning.

Jeffrey A. Ryan and Joshua M. Ulrich (2020). quantmod: Quantitative Financial Modelling Framework. R package version 0.4.18. https://CRAN.R-project.org/package=quantmod

R Core Team (2021). R: A language and environment for statistical computing. R Foundation for Statistical Computing, Vienna, Austria. URL https://www.R-project.org/.

Marek Hlavac (2018). stargazer: Well-Formatted Regression and Summary Statistics Tables. R package version 5.2.2. URL: https://CRAN.R-project.org/package=stargazer

van der Loo M (2020). tinytest “A method for deriving information from running R code.” The R Journal, Accepted for publication. <URL: https://arxiv.org/abs/2002.07472>.

Yihui Xie (2021). knitr: A General-Purpose Package for Dynamic Report Generation in R. R package version 1.33. https://CRAN.R-project.org/package=knitr